|

|

|

March 13th, 2007 at 08:56 pm

Text is I was waiting for this... and Link is articles.moneycentral.msn.com/Investing/Dispatch/070313markets.aspx I was waiting for this...

Fortunately it still looks like we'll both be employed for the next year, and kindergarten is promising to be lighter on our pocketbooks than $910/month preschool. Another goal could be to save six months' mortgage expenses somewhere outside retirement.

Does anyone know what happens to privately owned mortgage lenders, like regional thrifts, who aren't dabbling in the subprime market when this happens? They'll probably have to tighten their lending standards too, but what else? They're not publicly traded.

I wonder if CDs, gold, and treasury notes and bonds are the way to accumulate cash in taxable accounts so as to pay off mortgage early. I know, Text is "it's risky and bad planning to have too much of your net worth in your principal residence." and Link is www.moneyweb.co.za/mw/view/mw/en/page94?oid=79089&sn=Detail "it's risky and bad planning to have too much of your net wo... Right now 49% of our net worth is tied into our principal residence. I feel bound: banks have taught me not to think I can profit i them, stocks are manipulated, bonds might be a sucker's game if they're issued by a debtor nation... what else is there to invest in?

I wonder how else I and my husband could protect our family from this. I wonder why people and companies never ever pay attention to economic cycles and history, or know what follows a boom. Have so few people ever rode a rollercoaster? Ever wonder if bank execs binge and purge or do yo-yo dieting the way they yo-yo mortgage lending requirements?

Posted in

|

1 Comments »

March 11th, 2007 at 05:12 am

Thanks all for your responses and commiseration to "when are you having another kid?"

I went on a spree of sorts with the family: we bought a battery tender to work with both our scooters, 20% off. We enjoy supporting our local motorcycle accessories shop: they make shopping great. Received free faceshield cleaner.

Bought at JC Penney a twin comforter (down alternative) for the boy, as we had only hand-me-down blankets, which made me think that if any visitors saw his room, they'd be calling Child Protective Services ("I'm serious! the blankets don't match! they're older than he is!") and a 330-thread replacement set of sheets for our bed, both for slightly less than 50% the regular price.

The frugal thing to do would be to NOT buy the Battery Tender, but juicing up the bike with the car isn't always a viable option, and doesn't restore the battery beyond 80% power. That's cheaper than buying a battery every twelve-eighteen months though. I dislike the backfire of the idea that scooters will save money: I've spent money on boots, helmet, super-reflective vest, helmet halo, battery tender, maintenance. No modifications for aesthetics or warmth. At least I vanquished the temptation to buy an extra set of cold weather gloves ("if you ride for two hours in temps below 50F your hands will get cold no matter what!" said my expert friend).

I learned through my scooter battery experience that although every rider asserts 'it's always the battery' everyone has a different idea of solving the problem. Buy another battery. Check the fluid. Take it in for inspection. Jump it with a car and ride around for two hours. Buy a battery charger. I paid most attention to the Sound Rider! guy who said that scoots like mine don't like the cold, and yes it was 32F the day my scooter said 'hell no! You can't make me go!', so maybe the cold weather got it down.

Then we ate at a neighbourhood Italian comfort food restaurant with organic food. No wine. Kid was bratty-tired, but thankfully the restaurant had a corner of toys and amusements for the children six and under, so despite our limited patience with our squirmy whiny bundle of joy (yes we made absolutely sure he wasn't bothering the other patrons--we may be parents but we are conscientious and not oblivious), we'll be coming back.

Tomorrow I hope to earn six hours' overtime.

Eventually we'll sift through our linens and donate the excess: maybe three lucky homeless people out of over two thousand will have an extra layer to protect them from the elements.

My spouse did not receive WARN (Worker Asset Reduction Notice), either in writing or by telephone, so he's still employed. I guess that's good: he has excellent benefits and can continue to work at home at a schedule that accommodates our household. Too bad he has work pressures. His company's execs are creaming themselves talking of outsourcing and reduction in force. Except outsourcing of executives. Interesting how that works.

Posted in

|

0 Comments »

March 10th, 2007 at 01:02 am

Mindboggling.

Answer: "One's all I need to be a parent. One's all I can comfortably afford."

"Why? Do you and your husband work at McDonald's?"

"Daycare is $900 a month."

I don't really feel like saying we can't afford to live here on my husband's income, nor do I feel like explaining that he doesn't feel any impetus to earn more money, or that I earn in any given month 80-120% of what he earns: being a single wage-earner family would be a big drop. I usually shoot back: "are you going to pay for it?"

Usually the people who ask me why I don't have more children are the people who gripe about families breeding more than they need to/can afford. Or are from countries with subsidized daycare. Or are in their sixties.

Posted in

|

15 Comments »

March 9th, 2007 at 11:29 pm

Before interest-only and option ARMs, before thirty-year mortgages, before subprime credit card companies like Providian and Aspire, even before Social Security, Americans had different ideas about saving, thrift, debt and credit.

Myvesta.org presents for our viewing pleasure Text is ephemeral films and Link is http://www.myvesta.org/films/ ephemeral films.

Also, from Text is Get Rich Slowly and Link is www.getrichslowly.org/blog Get Rich Slowly see a link to CNN Money's Prioritizer tool. My five money priorities:

1. Save 10% of income for retirement, as Social Security's supposed to be wiped out at 2042.

2. Save for new windows for house.

3. Save $3600 for summer vacation.

4. Save for new roof for house.

5. Save 30% for replacement car downpayment.

I recorded two spreadsheets, one for what I could expect if social security were still around for me (HAHAHAHAHAHA) and one if it weren't. I'm slightly behind in the second scenario, expecting to live on 52% of our current income (no daycare, no mortgage, that combination is 48% of our expenses).

Posted in

|

1 Comments »

March 9th, 2007 at 08:15 pm

I found a Text is local debt blog and Link is www.debtinseattle.com local debt blog and am tempted to invite the woman to our debt support group meeting tomorrow. So refreshing to find Seattleites who save and live on their earned income.

I was feeling all punk and angry about my $169 natural gas bill in January -- I know, get the film for the windows, feel for drafts, do an energy audit, I do read the blog comments -- but that's a trifle compared to a $480 gas bill like the author of Text is Debt in Seattle and Link is www.debtinseattle.com Debt in Seattle has. She has three little ones. I have one little one. I'm trying to teach him to suck it up and be Canadian about colder temperatures. "When I was your age I had a SNOWSUIT! You've never had one! It got so cold out some days we had to stay indoors." Ah yes, memories of ice fishing, snowshoeing, and skating on frozen-over lakes: REAL WINTER.

I saw on Text is Heating Degree Days and Link is http://www.seattle.gov/light/ddays.html Heating Degree Days the months and their temperatures' differences from a set temperature. There's some ratio calculated where the fewer days with temperatures below 65 degrees, the warmer it is. Degree Days also indicate possible explanations for not seeing predicted savings from weatherization work. With an energy rate increase and cold weather and power outages from a bad winter, what would make me expect savings from keeping the thermostat at 58F at night and 64F during the day?

I tend to forget that my gas bill comes to $15 in the summer months.

Posted in

|

0 Comments »

March 8th, 2007 at 09:55 pm

Eight windows, two of them very large (living room). Guessing $375 - $500 for each window, plus tax, plus 15% for contingencies: $5000.00. Somehow I sense it'll be much more. The two windows in our bedroom cost $2000.

I can risk $6000 from the HELOC.

Told Lord and Master I'd feel better with $5000 in savings (not locked up in CDs), and having the tax bill paid prior. I want at least one-third of the cost available in cash before going forward with the work.

low U-factor, under 0.35

high solar heat gain coefficient

argon gas fill

west windows: three

east window: one

-- SHGC lower than 0.55

south windows: two

-- SHGC high

-- U-factor under 0.35

I don't know how to get technical information from the manufacturers' websites: I'm looking at Marvin, Lindal and Andersen.

Posted in

|

3 Comments »

March 7th, 2007 at 11:43 pm

Whew. It won't reach my brokerage until next week, but still, there's something celebratory about squeezing in that last payment.

An oops though, I've contributed $3250 already. Perhaps the brokerage'll move $150 to the 2007 contribution.

Ten months at $400/month for Roth IRA 2007 contribution.

I bought a $500 CD with a $500/month "add-to" feature. In retrospect I think this might be a bit much. Then again, it depends on what the end expenditure will be: windows, a car, vacation...

Posted in

|

3 Comments »

March 6th, 2007 at 05:31 am

Text is Betweem Two Rivers Scooter Calculatorl and Link is www.btrscoots.com/scootcalc/ScooterCalculator.htm Betweem Two Rivers Scooter Calculatorl allows me to get a better idea of what impact my scooter use has on the environment and the economy.

Here's some of the result:

you burn 107.14 gallons of fuel in your Yamaha Majesty each year, and that amount of fuel costs you $277.50. In your other vehicles you burn 88.89 gallons of fuel, which cost you $230.22.

If you did not have your bike, you would be forced to put 10,000.00 miles on your other vehicle each year. This would cost you $959.26 in fuel charges each year. Having your bike saves you $298.06 in fuel costs each year.

If you did not use your bike, you would burn 370.37 gallons of fuel, but with your bike you only burn 255.29 gallons of gas each year. Therefore, using your bike conserves 115.08 gallons of gas each year. Translated into barrels of oil, that represents 5.48 barrels of oil that did not need to be refined for the gas you used.

If 1,847,820 people in this country rode a scooter like you, an entire day's worth of oil imports into this country would not be required, resulting in more than $500 million dollars that the country would not need to devote towards foreign oil purchases.

The goal for the planet is to reduce our energy use by 80% over four decades. This is a decent start. Of course, if I rode a smaller scooter or a bicycle, the savings would be greater.

I also had a no-spend day.

Posted in

|

4 Comments »

March 1st, 2007 at 07:12 pm

Today I start writing down everything I spend money on.

It feels good to have a month's planned expenditures in a chequing account.

Yesterday I told the lads that we are scrimping $500/month to be set aside for the purchase of a recent vintage automobile. Our car is now exactly at 130,000 mi. We've owned it for nine years. Contrary to my born-again "green" attitude, I am considering, among the Toyota Prius, a Honda Accord, Toyota Camry, Volkswagen Passat 3.6, or a BMW 325i, as we have several low-fuel or no-fuel commuting options: carpool, flexcar, motorscooter, bus, bicycle. I want an automobile only because we do get foul weather on occasion--it snowed here today--and I have a small child who justly does not feel safe riding behind us on our scooters, and there are times I tote more than just drycleaning/librarybooks/3bagsgroceries. I'm not going to keel over and die in a messy pool of guilt because my car gets only 24 mpg when our other self-commandeered options get 80 mpg and 55 mpg and more use out of them -- we don't drive our kid to many places other than friends' birthday parties, appointments outside the city, or roadtrips.

My husband was asked why we don't have two cars. Since 2001 we've been bouncing around from having one to two cars in our driveway: I don't really buy cars, I just 'rent them' or 'maintain them' while their owners are overseas. They're expensive to insure, feed, park and maintain.Driving is actually more pleasant now, because I don't have that defensive "everybody hates me and my fuel efficient freedom, I must protect myself from jealous killers who pretend to be oblivious with their Blackberries and cellphones" mantra behind the wheel that I do on my scooter.

Today also in earnest I start planning for what could be the first and last major roadtrip we take as a family this summer: a cruise down as much of Highway 101 as we can. I'm budgeting $3400 for twelve days. It'll be like Steinbeck's 'Travels with Charley.'

I will buy the Consumer Reports April Auto issue, or look at it in the library.

I am $900 away from maximizing my Roth IRA contribution for 2006.

I ordered seed catalogues from Landreth, Seeds of Change, Territorial Seeds, Abundant Life, and Heirloom Seeds. I saw an article on MotherEarthLiving.com about the ten best beginner crops and really just want to stick to herbs and a handful of vegetables: green leafy sturdy varieties; tomatoes if I can.

My wackiness for this week is 'how to apportion out the overage to crawl toward my individual savings goals.' Better than last week's quarterly neurosis of 'I am going to live my life in poverty'. My husband said I should be happy that I fared better than my parents but gee, isn't faring better than dysfunctional high school dropouts who spent most of their lives in the poverty line a low expectation?

I saw that the energy credit for windows tops out at $200. Not quite the heftiness of the solar energy credit. I know I've posted before about the question of energy savings using solar energy. Now, I am concentrating on windows. We'd been wanting to finish up our windows replacement from two years ago.

I must remember that if I sink because of deflating home equity and mutual fund NAVs, so too do my friends and associates.

Posted in

|

2 Comments »

February 27th, 2007 at 08:56 pm

I am diversified, perhaps improperly. And no gold or silver yet.

Text is Generation X Retirement Calculator and Link is www.retireearlyhomepage.com/software.html Generation X Retirement Calculator: feeling MUCH BETTER about retirement now.

457

Equity style pct.

ARTIX international 6.0%

ARTVX small value 4.5

RPIBX int'l bonds 5.8

RPMGX midcap growth 4.6

PTTRX bonds 4.4

VINIX S&P index 4.5

Roth IRA

PAYX Paychex stock 1.9

PHO Water ETF 3.3

PID intl stock 2.9

VDMIX dev mkts 6.5

VFIIX GNMA 4.9

VGSIX REIT 5.0

VISVX small value 4.9

VIVAX index value 6.6

VTRIX int'l value 5.0

Cash 3.0

Rollover

EFA EAFE index 2.1

QQQQ Nasdaq ETF 1.9

SPY S&P ETF 4.1

MVALX midcap value 4.5

VFSTX short-termcorp 6.0

VGTSX total stock 8.9

In retrospect I am glad I didn't yield to the temptation of PowerShares Golden Dragon China ETF.

Posted in

|

0 Comments »

February 25th, 2007 at 02:14 am

I flip through the excellent Your Money Or Your Life. I have lost sight of what "enough" is. I supposedly need $889,153 by age 68 for retirement, but what's meant by 'enough' is when it's fruitless to continue the grasping and building to keep up with someone who's always going to have more -- this trap I fall into too often. Accumulating for the sake of accumulating isn't healthy.

I need to sit down with the lads, talk about our tax situation, what money goals we have, how to make them realistic, and what we're going to do to meet them. And maintain that perfect fabulous balance of being sufficiently covered for liquidity and on track for retirement. As someone said, "you can have it all, you just can't have it all at once." What I want: a car fund, a vacation fund, and new windows.

Feeding the poverty neurosis: I opened an account at a new branch of a credit union so I could get a safe deposit box. I gave my driver's license, they did an online check of my banking activity and I was told "all we can give you at this time is a savings account."

This is how bad my banking has to be to be initially offered only a savings account at the credit union:

� be a joint mortgage holder with 94 months of on-time payments;

� two brokerage accounts 8 years and 4 years old but low;

� three retirement accounts nine, six and five years old respectively;

� joint chequing/savings account combination of $10K in assets;

� another chequing/savings account: very low -- wanting to move out of that.

� one joint personal line of credit unused for two years;

� one joint home equity line of credit not yet used;

� three credit cards: eleven, seven, and five years old respectively all with ontime payments;

� own your vehicles in full;

� demonstrate a record eight years long of paying off your vehicle loans early and ontime.

So gosh, how loaded do I have to be to satisfy opening a mere account? This isn't an illegal alien opening a Bank of America credit card account! I've legally been in the country for over ten years and contributed in many ways to the economy and tax base through consumption and income!

Or maybe you just have to be a permanent resident to be deemed unworthy with the above. I wanted a business account and an account where I could use electronic funds transfer to my Roth IRA, because I can't do that with my joint account.

So I protested. they needed to see my Social Security card, because apparently I've been in 'cahoots' with someone with a different SSN (like, my husband?) in financial dealings. Gotta love that Patriot Act. I did get a chequing account, finally, just like I did when I didn't have credit to begin with, or even my Green Card yet, and when I did with two other credit unions. The person who helped me open my accounts apologized.

Posted in

|

2 Comments »

February 23rd, 2007 at 09:11 pm

Eight years ago today my mother died. I learned last night a friend's mother died. She and I both shared the thought "are we now the self-actualized women our mothers wanted us to be?" And I'm reflecting. Am I in a good position? If yes, why do the green meanies consume me?

I was shown an internet comic strip where in the first panel are people queuing for a "one wish per lifetime per customer" wishing well, their wishes written on slips of paper. A man throws in a paper with "True Love" and a blonde woman in a pink dress is at his side instantly. In the third panel he sees other well-wishers: one carts a huge stack of money in a wheelbarrow, another has his own sci-fi fighter jet, a third flies away in a Superman costume. The fourth panel has the true love man slapping his forehead, trundling dejectedly down the hill with his true love.

Gail Sheehy says: "It's much more fun being the aspirant, because once you have gotten [instant wealth], even if you are just there temporarily (as you must continually remind yourself you are), you're in a position of defending or protecting rather than aspiring or building.

"It's terribly uncomfortable. It's also a problem that is totally unsympathetic to anyone who has five cents less than you do. Right? So there's nobody you can talk to."

Posted in

|

2 Comments »

February 23rd, 2007 at 03:31 pm

I have PostPoverty Stress Disorder.

I had a "math crash" figuring out the bill at a restaurant, which made my friend snappish and belligerent (I also didn't join her in a cocktail either). Sometimes all it takes is to ride in someone's BMW, or hear about a vacation, or how my kid's peers are being sent to private schools, and I fall prey to the sin of covetousness. 'Cause my friends have no kids, and parents who actually owned property and had assets. They can relax.

For instance: For the past nine years I have wanted to go to Hawaii for winter. It burned to hear other mothers talk about their upcoming Hawaii vacations.

I talked to my spouse and he told me for many years he had to stay home while his friends and classmates flew to Disney World or Disneyland. Our plus-kid trips are typically to see my spouse's parents, or they are drives to Vancouver BC or Portland OR. We reminisced about the trips we took nine years ago when our rent was $600, our salaries were half of what they are now. Our net worth was $9000 when we took those trips, tops. Mortgage, sans real estate tax and insurance, is twice the rent. Our net worth, $440,000. The lads went to visit my in-laws, who do not live in Palm Springs or Waikiki. They're temporarily infirm, so their getting over here is not feasible at this time.

The sad thing: our kid actually has it pretty swell compared to what we had at his age. Both our sets of parents were still renting. He hasn't moved three times like my family did. He has a college fund. We don't eat marshmallow fluff for three days because that's the only thing in the house. A BIG trip for us was to a city 150 miles away. He even has a set of parents who like each other and don't have a dysfunctional relationship. Dammit, why isn't this enough for me?

Instead of hearing from my aunts how their daughters are getting ahead "upgrading their spouses" and relying on the spouses to bring home the big bucks and making me feel like a dumbass for earning my own money and not relying as much on my husband, instead of reading "maybe cut your cell phone or get rid of your cats" for budget recommendations I just want to read that yes, the first five years of parenting a child are costlier than normal, there's light at the end of the tunnel. And to be reminded that our mortgage term is shorter than the terms of other families, so we're building equity faster. And it'd help if someone would virtually pat my hand and say "oh sure, putting in 10% with an employer match in your 401(k) and budgeting to fit in Roth IRA maximum contributions will pay off in the long run, more than sweet memories of sipping cocktails on a beachfront deck watching the sun set over the Pacific when you're in your 30s, and come to think of it, going from $9K to $440K in nine years isn't the crappiest thing ever."

Posted in

|

13 Comments »

February 19th, 2007 at 11:25 pm

Harvard Professor Elizabeth Warren, whose blog I visit occasionally, was referenced in a Liz Pulliam Weston article as offering a 50% after-tax rule for middle-class families spending on the combination of food, shelter, insurance, childcare, and transportation.

For this Seattle family that is $500, $1430, $90, $910 and $220 ==> $3150. After tax that's 50% of $6300 after tax, which would be about $9900 before tax. In actuality there's a dependent care spending account benefit so maybe $500 out of pocket post-tax: $2740. Still, $5480/month, yeesh.

I had budgeted $4280/month. The spouse brings home $3000/month after taxes, 401(k) contributions, dependent care. Tell us we're spending too much on housing? We've got a 5% for 20 years and $250K in equity: no way are we going to refinance. $220/month for transportation for three vehicles -- expensive? No. Food we could cut down on, that's a gradual process. And childcare, well, that's greatly reduced in September, we have to wait that out.

And Prof. Warren thinks this is doable? I could understand why, if the median debtload is $86000 (including mortgage). I'm going to be in my 40s by the time our debtload goes down that far. Then again, 1-bedroom condos in Seattle go for the cost of a median SFH in America.

My first paycheque is going to be meagre, but I'm hoping to net $1000/week after.

It feels like a struggle to stay in the middle-income segment here. At least I can look at "Your 30s: Now's the Time to get ahead" and not feel I'm so badly off. And who knows, if someone can look at what I post as a typical family attempting to get by without stock options or big inheritances and understand it to be reality, rather than a severe deviation of the norm, that'd make me happy.

Update: read this bit from a Seattle P-I sound off, a parent and homeowner surviving on $130K in Seattle:

"We can afford to go on vacations to Disneyland or even Hawaii almost yearly and we are definitely not the coupon mongering, save every penny types, though we are pretty vigilant about putting at least 10% of our annual income into a retirement account."

And that's with two car payments too. Then again, the children are elementary school age and not costing $1000/each/month in childcare.

I gotta think about what it is we're doing wrong.

Posted in

|

6 Comments »

February 17th, 2007 at 01:38 am

Not since Nov 2000 - Jan 2001 have I been this obsessed about heating bills. Our next heating bill is at $179. Sunday is the heaviest use of gas in our house.

Yesterday I fiddled with the thermostat settings and thought if I turned the heat off at night we might save some dough. My spouse shouted/argued with me for five minutes instead.

"I don't want high heat bills," I said.

"If the rates go up we're going to pay more."

"Which is why we should use less," I counter.

"I've not been taking the car out so much," he said.

"It doesn't feel that way to me. I seem to be refueling every eight-nine days," I said.

"Cars lose fuel efficiency in the winter," he said, "and the car was being refueled every 4-5 days."

Yikes. $165/month. I thought it was $120. Now we're spending $100/month on gas, altogether for three vehicles: $75 car; $18 big scooter; $7 scooter.

I wonder how much pressure I can apply on him to have our windows replaced. I read here about people with $120/month heat rates and I seethe with envy, but not enough to make my husband warm.

Then again, my electricity bill comes to $25/month every month, and I bet in the south and east the summer bills for electricity are much higher.

But you know, even the President, the guy who said "I encourage you all to go shopping more," wants a 20% reduction in energy usage. I don't want to waste energy. I want to be a good citizen.

Posted in

|

6 Comments »

February 15th, 2007 at 06:06 pm

If you can call laundry, menu planning, and rose pruning "freedom." We can be jolly and say "you have land and roses for a beautiful summer," "you can pay for utilities," "you have food with which to plan meals" and get our attitude of gratitude out of the way early.

I bought 100 shares of PID (PowerShares International Dividend Yield) this morning. I'll be photocopying my taxes and schedules, sending away for a citizenship certificate for the lad, listening to vintage jazz and cleaning up.

I learned that although my contract's 401(k) fund options are sucky (below average performance, only one index fund option for a category I'm already overweighted in, 12b-1 fees, front load fees: ick ick ick), my 457 plan allows for rollovers! So I can just pile up cash without investing it in anything other than "Stable Value" for a year, get a company match, and then roll it into my most excellent 457 plan. Or maybe into my Rollover IRA, which has all of one cent in cash.

I also did an energy audit for the home. We're using much less electricity than other homeowners, somewhat less water than

homeowners, but we're dead average for natural gas usage. This concerns me. I'll have to play with the thermostat some more. On with the windows research!

So no exemptions for the job, 10% 401(k), medical deducted at $63/pay period. $1200 Roth 2006 contributions remaining, $872 due April 17.

Posted in

|

0 Comments »

February 15th, 2007 at 03:11 am

God must have enjoyed riding pillion with me through north, mid- and south Seattle today, for I was blessed with the crazy thought of doing my taxes again.

I had asked my friends for recommendations, but surprise! the CPA recommended was booked until April 17. I inwardly sobbed for thirty seconds, then bucked up and took another whack at the 1040.

Yes I still owe. No, it's not $5600. It's $872. I used the computer calculator, and not a beverage napkin this time. I had some Talk Talk playing ("Missing Pieces") and was enjoying some fragmented 'bliss out' moments that come after an extended tour ride on the scooter. I miscalculated initial wages, the Dependent Care benefits declaration was new, and I didn't include the Child Tax Credit in my first pass either. I also saw I could deduct my business license expenses.

But $872 is very manageable. I can save for that in two months no problem. It's also under 10% of the total tax withheld too, so no penalty!

Posted in

|

4 Comments »

February 14th, 2007 at 01:07 am

I'm hoping I've overadded the wages, and underadded the deductions: it looks like we may owe $5600 beyond what we withheld. As we probably won't be assessed a penalty (our taxes are WAY Beyond 2005, the second of two conditions required for nonassessment of penalty), it doesn't seem that bad, and it's preferable to having money returned to us by the government, but OW.

As in:

we don't have that in savings yet OW.

"but I was gonna feed my Roth with our existing money" OW.

"but what about replacing the windows this year?" OW

"I thought we saved more money last year" OW

We didn't save much money in 2006. I paid off my scoot, we paid $1600 in damages incurred on a rental scooter my spouse commandeered and crashed, $1100 in dental services for our child, $1400 in motorcycle gear for the both of us, $900 on updating the wardrobe, $1100 on a brake job and service for the car, and fed $5500 to my Roth. I also overpaid our mortgage principal by $1300. All of this: aiyee.

I feel I've been obliviously wasteful. Especially since I'd been doing things like abstaining from using the car, choosing more fuel-efficient transportation, holding off on getting cellular phones, taking on extra jobs. Being free of consumer debt is little consolation.

Because now I can see it's only a matter of how long a string of emergencies could be to bring an otherwise doing-okay family into debt: car breakdowns, accidents, medical crop-ups, sudden family deaths, disasters affecting the home. You can't schedule these for the convenience of your emergency fund!!

And before anyone gets any holier-than-thou "I always plan my exemptions" thoughts, let me explain that I was a stay-at-home mom for 20 months before returning to work for a two-month contract in November 2005 that was renewed every two months, and I was ignorant of the return of the strong job outlook in my dotbomb environment. I didn't know how long it would take for me to find my next contract.

So I don't want to do the taxes this year. Let some impassive third party go through my life, tightlipped and poker faced, and deliver the result to me.

Posted in

|

5 Comments »

February 11th, 2007 at 04:05 am

I would like solar panels on my roof. We looked and although our HOUSE doesn't face south we have lots of roof space facing south. If we buy them this year we get:

[list]

[*] a tax credit for 30% of the qualified solar-system expenditure (must produce 50 percent or more of the hto water needed)

[*] no sales tax for OG-300 rated solar heaters.

[*] every dollar I spend on this system will be added to the home's value when I sell.

[/list]

So if we use our home equity line of credit for this, amd we can pay it off in a year, I'm going to pop for solar. The downside is that I'll still be dependent on natural gas in the winter months of Sept-March.

I want the windows done first though. Still. Years overdue for replacing the rest of the windows, and they'll make a little difference in heating the house.

Posted in

|

4 Comments »

January 31st, 2007 at 03:52 am

January is the hardest month financially for my family. Water/sewer bill, electricity bill (a third of the water/sewer), highest natural gas bill, semi-annual insurance, dental appointments. I start to worry about making my full Roth IRA payment, and fret about energy. I'm reeling from some poorly timed purchases: pricey motorcycle boots, dresses for interviews, another motor scooter (80 mpg, under $2K), a nifty helmet.

For those who keep track, I am in my quarterly "I am poor and inadequate and have no self-discipline, so I'll throw myself under a hybrid bus" anxiety attack.

Especially I am fretting now that I'm reading High Noon for Natural Gas by Julian Darley, and The Party's Over by Richard Heinberg. I live in the Pacific Northwest, and ten months of the year being here is splendid. This is not one of the splendid months ($147 heating bill).

How do I calculate the projected natural gas costs? I need to estimate them so I can determine if it's worth going back into debt to make energy efficient home improvements, or if I should just use some film coatings and caulk.

There are simple living groups and gurus (Cecile Andrews, Vicki Robin, Steve Rose all live in Seattle), study groups and progressive communities here, including a Peak Oil Awareness group. They're probably all debt-free with no mortgage, or child-free. It sounds hokey to put out a personal ad, but I'm wondering if there are any other parents nearby like me who are thinking "eeps! I better adjust so I can give my kid and my senior self a better life!"

Thursday's Peak Oil Awareness group might be where I meet him or her.

When the World is Running Down, You Make the Best of What's Still Around

I sometimes fear I'm unwilling to make necessary adjustments to adapt to the reality of diminishing oil and gas reserves -- this year so many countries (Canada and Mexico and others) are to have their peak output of these natural resources, and then trouble will start (like it didn't start in 1973, or 2003).

I have strong psychological attachments to the home, I don't have the time right now really to get gung-ho on gardening, aside from ordering seed catalogues from organic seed suppliers. But I have Steve Solomon's book Gardening When it Counts.

Something else I need to do is rely more on beans and rice to make complete proteins. A few months ago, inspired by the peak oil crisis, I opted to make as much of my diet come from agriculture within 100 miles from me. I eat more fish than chicken and beef these days, but a recent New York Times article by Michael Pollan gave me twinges of regret spending $100 on local organic beef and wild-caught fish this past weekend. Our diet should be mostly plant-based, with maybe a 4 oz. portion of meat, instead of the 5-6 oz. portions. I'd save some dollars.

And I did a bad thing -- I walk close to a mile every day, either to the post office or bus stop or library. Sunday afternoon, jonesing after taking my tot for a 1.3-mile walk with playtime around a man-made lake, I took my motorcycle to the library (0.5 miles away) to photocopy the Sunday crossword. That cost me nearly five cents in gas. I could have walked some more, but seeing other motorcyclists enjoying the sun makes me itch for my scooter key.

It is not without alarm I read online economic data points spiced like projected home valuation depreciation, current negative savings rates, with the comment "Not since the 1930s..." Everyone knows how America fared in the 1930s, right? At least I still have those bottles of sloe gin and liquors. And a fur coat.

I've got to cut down on the frivolous expenses, and I've got to get my family to help. I've got to increase our taxable assets, maybe buy some gold. And chickens. If S. J. Perelman, Dorothy Parker and Alan Campbell, and E. B. White can transition to farmer scribes, I should be able to transition to farmer tech scribe.

I want to inoculate us against the myopia and ignorance of others, and the waste and dystopic zeitgeist around me. I want to seek local versions of the SavingAdvice.com mentors here. I'll even make tea biscuits and offer what I hope to be the last frivolous purchase in a while: specialty tea from TeaCup. Even if it means turning on the natural gas to heat the water.

Protecting the family from screen media is another hard task. I rented "Mr. Show", Seasons 1 and 2 of a hip, long past (1995-1998) sketch comedy HBO show. My kid loves DVDs and VHS, although he sees maybe two hours a week, and we're thinking even that's too much for him: "Let's play Trailer Park Boys, okay? Let's play Mr. Show and I'll be Bob Odenkirk, okay?"

I need to lighten up, but at this point I am racing around the house yelling at people for leaving lights on. I need to break free of this bulimic pattern of scrimp scrimp SPLURGE SPLURGE scrimp scrimp scrimp. I am seriously considering giving up the television, only how would I watch my Chaplin DVDs at those times the world seems especially oppressive and pugnacious?

Posted in

|

1 Comments »

January 13th, 2007 at 04:46 am

Just so you know: I do not hate television. I own a television. I watch DVDs and videocassettes on average of three hours a week. Last week I watched "The Ben Stiller Show DVD." When I go to other people's houses I do not bitch about their television, nor comment on what they watch, nor how many they have. In short, I'm not disruptive, expressive, or rude. I accept the television's place in modern-day family homes.

I am puzzled at my severe dismay about a second television set entering the premises of my favourite cafe, which until last Sunday I adopted as a sanctuary, a home away from home. I had my kid's birthday party there, I spent twice my annual electricity bill amount there on coffee and other treats, made friends there, brought friends there.

There was a television in the back, up some stairs. On or off, it didn't bother me in the slightest. I could stay downstairs if it was on and if it was something I didn't want to watch.

Now I have this curious feeling of intrusion and betrayal because of the television screen added to the main area of the cafe.

Colman McCarthy, professor at Georgetown University and the University of Maryland, explains, "It is a commercial arrangement, with the TV set a salesman permanently assigned to one house, and often two or three salesmen working different rooms." Dr. John Condry, professor of human development and family studies at Cornell University, writes, "The task of those who program television is to capture the public�s attention and to hold it long enough to advertise a product."

I may be feeling out of sorts because I know the cafe is cutting costs, and is having emergency incidental expenses, but the television and microwave oven (a cooking component of the cafe) can't coexist peacefully: the amperage isn't enough for both.

I'd rather the cafe get on its feet, and spend on advertising its own assets and features, rather than buy a set that advertises other products.

Why do I feel like this? Why am I irritated to see the television in elevators, public government waiting lobbies, family restaurants?

Posted in

|

7 Comments »

January 11th, 2007 at 03:37 am

I learned of Text is "Turn off your TV" and Link is http://www.turnoffyourtv.com/radio/ "Turn off your TV" in August 2006. I didn't share it on this blog because it seems to me many, many Americans don't necessarily agree with Ron Kaufman's progressive point of view, and even I get tired of what I contend are obvious liberal political harangues: I see many harangues as polarizing, grandstanding and dividing the country from solving the issues that are urgent but not necessarily disseminated properly in the news, ESPECIALLY television. I'd rather everyone from left or right who earns below $150,000 a year listen to the podcast, and join me in heeding Ron's new year resolutions:

1. Defy the president's exhortation that "you all go shopping."

2. Look at your house as a home, not as an investment.

3. Make energy-efficient purchases.

#32 (January 2, 2007: "2007: The Beginning of the Slowdown") is a good, well-researched podcast. Heck, this even has a sound quote from DAVE RAMSEY, another from Class Warrior Steve Forbes, and yet another from FOX News: accessible sound bites for most, right? (actually, leave out that comma between most and right )

I figure regardless where your social mores and leanings lie, you want to protect your assets. You want to know what's coming so you can prepare. People with different social opinions from yours yet earn the same salary will likelily benefit from this info as much as you would, if they'd listen.

So for the open-minded, and of course for everyone who has a mortgage, a car, and an American job, I encourage you to listen to Text is Podcast 32 and Link is http://media.libsyn.com/media/turnoffyourtv/show32turnoffyourtv.mp3 Podcast 32 of "Turn off Your TV." So informative. So much the best of what Mr. Kaufman has released, in my opinion.

As usual, plan for the worst but hope for the best. I'm going to be moderate and cut my expenditures by 10%.

Posted in

|

2 Comments »

January 9th, 2007 at 07:41 pm

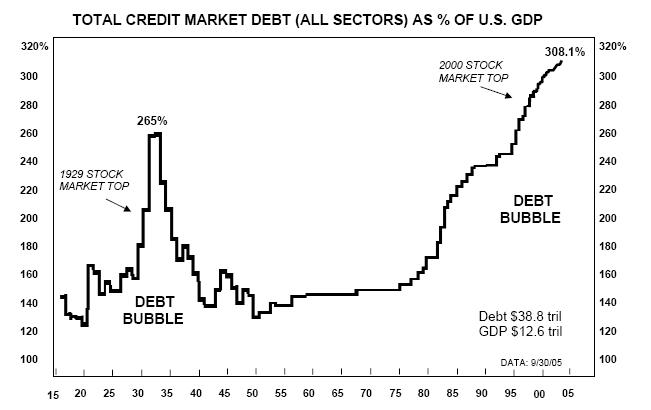

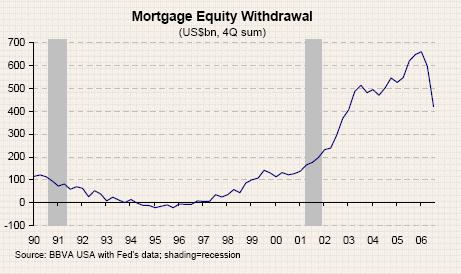

Source: Text is Sudden Debt and Link is http://suddendebt.blogspot.com/2007/01/some-rather-unpleasant-charts-chart.html Sudden Debt

The next chart shows how much money was taken out during the housing bubble in the form of equity withdrawal (the Fed estimates that 2/3 of this money was consumed - not saved). The amount is now going down fast and the impact is being felt in the retail sector.

I excised some text blaming the spending on plasma TVs.

Posted in

|

0 Comments »

January 9th, 2007 at 02:39 am

I checked Hugh Chou's Text is Retirement Savings Calculator. and Link is http://www.hughchou.org/calc/wealth2006.php Retirement Savings Calculator. For our age range, we're doing better than most retirement savers. We're not at the top end of the range (ages 35 - 44), so maybe we're doing better than 90% of the folks out there. 5% of the people in this group have $150,000 - $250,000 saved for retirement. And no, counting home equity for that is cheating.

We don't have mutual fund and stock brokerage account balances worth mentioning. Maybe I should start.

What's scary is looking at age groups beyond ours. Of all retired people, 20% have funds beyond $250,000. And we started to save only nine years ago. If we were smarter with our careers, and more driven and less poor, saving as soon as we got out of college and into those professional rather than support positions, we'd be surfin'! Our $$ includes the stock shock drops of 2000 and 2001.

Text is Hugh's got lots of calculators out there and Link is http://www.hughchou.org Hugh's got lots of calculators out there -- have fun.

Posted in

|

0 Comments »

December 30th, 2006 at 05:01 am

My spouse does not watch his 401(k) balance too often. When he asked me for help with asset allocation I thought I would swoon with delight and pride. I won't go into excruciating detail: I'll just say that, left unchecked for a few years, 67% of his portfolio went to large capitalization funds (!!!) and 9% was in bonds.

I advised him to be more equitable and conservative with his asset allocation categories -- he moved his percentages, double digits in most cases to index funds, and distributed 5% to "Stocks Gone Wild": Science & Technology.

I am breathing a little easier about possibly going into debt next year.

--------------------------------

My Schizoid Budgeting Style

* SpongeBob [my husband looked over my shoulder and said 'THAT'S ME! I AM SPONGEBOB!']: "WAIT! DON'T TELL ME!! You want me to run down to the store and buy Mrs. Puff something she doesn't need! Then you want me to run back here so you could say" (imitates Mr. Krabs and looks likes Mr. Krabs with the eyes), "'Arr SpongeBob, you're spending all me money!'. Then I'll say 'But Mr. Krabs, I'm only doing what YOU SAID!!!!!!'. Then you'll say we're not talking about this" (SpongeBob draws a square in the air with his fingers), "or this" (draws a triangle in the air with his fingers and starts to get frustrated), "WE'RE TALKING ABOUT THIS!!!!!!!!!!!!!" (He draws scribbles all over the screen until the whole screen is black).

Mr. Krabs [uh, me?]: But I really need this! (spongebob runs down and buy Mr. Krabs the item, and runs back)

Mr Krabs: YOU'RE SPENDING ALL ME MONEY SPONGEBOB!

Spongebob: But I'm only doing what you told me to!

Mr. Krabs: Well I can't help it, if you're loose with other people's money.

--------------

Gee, I wonder why my husband runs away when it's time for our monthly Finance Chat.

Posted in

|

5 Comments »

December 23rd, 2006 at 08:02 pm

Closed out my Bank of America checking account and emptied the safe deposit box I rented. No, I am not telling you where I live. I plan to move the contents to a credit union and rent its safe deposit box.

I was asked by the personal banker if I'd looked into other BoA accounts that would suit my needs. "This one suited my needs," I said, "and they're changing it to one that doesn't. I'm being forced to change."

I am sad that the bank's change in policy drove me out of my inertia. It likelily is just me, but my take was that the longer you are a paying customer, and the better your credit is established, the less the bank wants to change account terms to the point where it's disadvantageous for you to continue the relationship.

However, huge banks swallow smaller ones, not to continue the smaller banks' policies, but rather to feed on the plankton that is the customer base.

This is why I'm not in banking, and why I only begrudgingly use credit cards for convenience. Bank of America swallowed MBNA too, but MBNA was on a downward spiral when its CEO Alfred Lerner died.

I'm always torn about closing my credit card accounts -- there's no protection against a longstanding account being changed by the banking superGoliath into one that isn't quite so advantageous to the customer, so why chase after Visa, MasterCard, Discover, or Capital One? I had a Visa, then it was changed to American Express without my asking.

The ironic thing is that I saw local friends at the bank! My friend Susan, our mutual former coworker Curt (a personal banker there), and near the bank we saw a friend of my son, and the friend's father.

Banks can be good wealth-building tools, if you're a shareholder. So can credit unions, if you're a member.

I'll probably just buy a DRIP of Royal Bank of Canada (RY).

Posted in

|

4 Comments »

December 12th, 2006 at 08:30 pm

A friend sent me this Text is link and Link is http://www.latimes.com/business/la-fi-option11dec11,0,4921051,full.story?coll=la-home-business link to an article about an egregious case of a "pay option loan."

I suspect that newspaper journalists do seek out extreme cases such as these, leaving out salient facts like funding long-term care for parents, or fighting leukemia or AIDS for five years, that may change our sympathies, and we readers ponder: "Golly, how many people are there like this?" Me, I was floored there even was someone like this: a 56-y.o. man, twice-divorced, no kids, in a Covina CA house which he bought 11 years ago for $130K, filled with his stuff, and took $190K out of through refinances. Cowabunga, dude, get a roommate and put the additional rent income into your mortgage.

I took a second job to pump up my Roth IRA 2006 contributions, and told this to a fellow contractor. He confided he didn't have a Roth IRA set up, that the 401(k) thing wasn't a going concern as he had 25 years to retirement. We've got $163K in retirement and about 30 years left to go.

See, I'd have thought the earlier you pay into a retirement plan, the less you have to sock away in future years. These guys being kidless and spouseless have oodles of disposable income.

These are able-bodied and competent men, who've spent pretty much all their lives in the United States. What circumstances does one have to be nurtured in to trust corporate America with its offshoring jobs, layoffs, reduction of benefits, to think everything will be okay, that savings can always wait? Middle-class? Stable? Executive, VP or Board Director?

[hr]

from goldseek.com:

What will almost certainly go wrong is that the homeowners will have to cut back. Then, the lenders and hedge funds will be in trouble too. Get this - the last six years have seen the biggest property boom ever. Yet, the average American homeowner actually has less equity in his house than he did in 2000. What he has a lot more of is mortgage debt. And when his house falls in price, that debt is going to chafe his neck like a noose.

Am I in denial if I want to believe that the average American is not this ignorant or trusting to luck?

Posted in

|

5 Comments »

November 30th, 2006 at 05:36 am

So on some other community forum we tried affirmations. I have a neat little book Money is My Friend by Phil Laut with such affirmations. You choose a statement you'd like to self-program into your consciousness, write it out at least ten times, preferably in first second and third person, for a period of time. The experiment on the other forum was for two weeks, I should do mine for a month.

I may have timed my affirmation with a geyser of blessings: free latte from my fave cafe, a short-term stint very well-timed and very very pleasant. A month-long contract of decent pay but one bus ride away (and it's in town! No 90-110min commute from the Eastside!). And a possibility that's going to keep me doing these affirmations for another two weeks: at 150% of what I'm currently earning.

My affirmations?

I am highly pleasing to myself.

My connection to infinite intelligence and infinite abundance yields me a large personal fortune.

But I also like:

There are plenty of opportunities for me to serve people and increase my income.

and

The value of my work is increasing rapidly in everyone's opinion.

It's like, now that I'm not so angry-depressed-bitter, but energized-hopeful-subversive-progressive, the universe is rewarding me and encouraging me to keep on keeping on.

Posted in

|

3 Comments »

November 23rd, 2006 at 04:26 am

I'm grateful for my health, the local job economy, the advice I've garnered and implemented from this Website, a loving and mostly harmless husband, an adorable and bright son, my capable intelligent and supportive friends, and yes, begrudgingly I express gratitude for my early warning anxiety system, which gives me the energy to plan and stave off disaster.

New goals to save for, after the vacation in CA in August:

Cistern/aquifer installation and filtration system

Organic garden in backyard

Replacement windows

Fireplace inserts

Posted in

|

0 Comments »

November 19th, 2006 at 05:48 pm

From Rosemary Wells' book My Kindergarten:

Miss Cribbage asks me to write the number 95 on the board.

I can't do it.

Odysseus writes it instead.

I begin to cry. I have forgotten what every single number looks like.

Diane Duck and Louise sit with me until I stop crying.

"I do not want there to be any more numbers. There are too many," I tell them.

That night at home, Papa agrees with me about too many numbers. He sits at his desk and closes the checkbook and stacks the bills.

"When all the numbers in the world gang up and land on you, punching and crunching," says Papa, "it's called a math crash!"

"How do you fix math crashes?" I ask.

"I run around the house ten times and take a hot bath and they go away," Papa answers.

Posted in

|

2 Comments »

|