|

|

|

Archive for January, 2007

January 31st, 2007 at 03:52 am

January is the hardest month financially for my family. Water/sewer bill, electricity bill (a third of the water/sewer), highest natural gas bill, semi-annual insurance, dental appointments. I start to worry about making my full Roth IRA payment, and fret about energy. I'm reeling from some poorly timed purchases: pricey motorcycle boots, dresses for interviews, another motor scooter (80 mpg, under $2K), a nifty helmet.

For those who keep track, I am in my quarterly "I am poor and inadequate and have no self-discipline, so I'll throw myself under a hybrid bus" anxiety attack.

Especially I am fretting now that I'm reading High Noon for Natural Gas by Julian Darley, and The Party's Over by Richard Heinberg. I live in the Pacific Northwest, and ten months of the year being here is splendid. This is not one of the splendid months ($147 heating bill).

How do I calculate the projected natural gas costs? I need to estimate them so I can determine if it's worth going back into debt to make energy efficient home improvements, or if I should just use some film coatings and caulk.

There are simple living groups and gurus (Cecile Andrews, Vicki Robin, Steve Rose all live in Seattle), study groups and progressive communities here, including a Peak Oil Awareness group. They're probably all debt-free with no mortgage, or child-free. It sounds hokey to put out a personal ad, but I'm wondering if there are any other parents nearby like me who are thinking "eeps! I better adjust so I can give my kid and my senior self a better life!"

Thursday's Peak Oil Awareness group might be where I meet him or her.

When the World is Running Down, You Make the Best of What's Still Around

I sometimes fear I'm unwilling to make necessary adjustments to adapt to the reality of diminishing oil and gas reserves -- this year so many countries (Canada and Mexico and others) are to have their peak output of these natural resources, and then trouble will start (like it didn't start in 1973, or 2003).

I have strong psychological attachments to the home, I don't have the time right now really to get gung-ho on gardening, aside from ordering seed catalogues from organic seed suppliers. But I have Steve Solomon's book Gardening When it Counts.

Something else I need to do is rely more on beans and rice to make complete proteins. A few months ago, inspired by the peak oil crisis, I opted to make as much of my diet come from agriculture within 100 miles from me. I eat more fish than chicken and beef these days, but a recent New York Times article by Michael Pollan gave me twinges of regret spending $100 on local organic beef and wild-caught fish this past weekend. Our diet should be mostly plant-based, with maybe a 4 oz. portion of meat, instead of the 5-6 oz. portions. I'd save some dollars.

And I did a bad thing -- I walk close to a mile every day, either to the post office or bus stop or library. Sunday afternoon, jonesing after taking my tot for a 1.3-mile walk with playtime around a man-made lake, I took my motorcycle to the library (0.5 miles away) to photocopy the Sunday crossword. That cost me nearly five cents in gas. I could have walked some more, but seeing other motorcyclists enjoying the sun makes me itch for my scooter key.

It is not without alarm I read online economic data points spiced like projected home valuation depreciation, current negative savings rates, with the comment "Not since the 1930s..." Everyone knows how America fared in the 1930s, right? At least I still have those bottles of sloe gin and liquors. And a fur coat.

I've got to cut down on the frivolous expenses, and I've got to get my family to help. I've got to increase our taxable assets, maybe buy some gold. And chickens. If S. J. Perelman, Dorothy Parker and Alan Campbell, and E. B. White can transition to farmer scribes, I should be able to transition to farmer tech scribe.

I want to inoculate us against the myopia and ignorance of others, and the waste and dystopic zeitgeist around me. I want to seek local versions of the SavingAdvice.com mentors here. I'll even make tea biscuits and offer what I hope to be the last frivolous purchase in a while: specialty tea from TeaCup. Even if it means turning on the natural gas to heat the water.

Protecting the family from screen media is another hard task. I rented "Mr. Show", Seasons 1 and 2 of a hip, long past (1995-1998) sketch comedy HBO show. My kid loves DVDs and VHS, although he sees maybe two hours a week, and we're thinking even that's too much for him: "Let's play Trailer Park Boys, okay? Let's play Mr. Show and I'll be Bob Odenkirk, okay?"

I need to lighten up, but at this point I am racing around the house yelling at people for leaving lights on. I need to break free of this bulimic pattern of scrimp scrimp SPLURGE SPLURGE scrimp scrimp scrimp. I am seriously considering giving up the television, only how would I watch my Chaplin DVDs at those times the world seems especially oppressive and pugnacious?

Posted in

|

1 Comments »

January 13th, 2007 at 04:46 am

Just so you know: I do not hate television. I own a television. I watch DVDs and videocassettes on average of three hours a week. Last week I watched "The Ben Stiller Show DVD." When I go to other people's houses I do not bitch about their television, nor comment on what they watch, nor how many they have. In short, I'm not disruptive, expressive, or rude. I accept the television's place in modern-day family homes.

I am puzzled at my severe dismay about a second television set entering the premises of my favourite cafe, which until last Sunday I adopted as a sanctuary, a home away from home. I had my kid's birthday party there, I spent twice my annual electricity bill amount there on coffee and other treats, made friends there, brought friends there.

There was a television in the back, up some stairs. On or off, it didn't bother me in the slightest. I could stay downstairs if it was on and if it was something I didn't want to watch.

Now I have this curious feeling of intrusion and betrayal because of the television screen added to the main area of the cafe.

Colman McCarthy, professor at Georgetown University and the University of Maryland, explains, "It is a commercial arrangement, with the TV set a salesman permanently assigned to one house, and often two or three salesmen working different rooms." Dr. John Condry, professor of human development and family studies at Cornell University, writes, "The task of those who program television is to capture the public�s attention and to hold it long enough to advertise a product."

I may be feeling out of sorts because I know the cafe is cutting costs, and is having emergency incidental expenses, but the television and microwave oven (a cooking component of the cafe) can't coexist peacefully: the amperage isn't enough for both.

I'd rather the cafe get on its feet, and spend on advertising its own assets and features, rather than buy a set that advertises other products.

Why do I feel like this? Why am I irritated to see the television in elevators, public government waiting lobbies, family restaurants?

Posted in

|

7 Comments »

January 11th, 2007 at 03:37 am

I learned of Text is "Turn off your TV" and Link is http://www.turnoffyourtv.com/radio/ "Turn off your TV" in August 2006. I didn't share it on this blog because it seems to me many, many Americans don't necessarily agree with Ron Kaufman's progressive point of view, and even I get tired of what I contend are obvious liberal political harangues: I see many harangues as polarizing, grandstanding and dividing the country from solving the issues that are urgent but not necessarily disseminated properly in the news, ESPECIALLY television. I'd rather everyone from left or right who earns below $150,000 a year listen to the podcast, and join me in heeding Ron's new year resolutions:

1. Defy the president's exhortation that "you all go shopping."

2. Look at your house as a home, not as an investment.

3. Make energy-efficient purchases.

#32 (January 2, 2007: "2007: The Beginning of the Slowdown") is a good, well-researched podcast. Heck, this even has a sound quote from DAVE RAMSEY, another from Class Warrior Steve Forbes, and yet another from FOX News: accessible sound bites for most, right? (actually, leave out that comma between most and right )

I figure regardless where your social mores and leanings lie, you want to protect your assets. You want to know what's coming so you can prepare. People with different social opinions from yours yet earn the same salary will likelily benefit from this info as much as you would, if they'd listen.

So for the open-minded, and of course for everyone who has a mortgage, a car, and an American job, I encourage you to listen to Text is Podcast 32 and Link is http://media.libsyn.com/media/turnoffyourtv/show32turnoffyourtv.mp3 Podcast 32 of "Turn off Your TV." So informative. So much the best of what Mr. Kaufman has released, in my opinion.

As usual, plan for the worst but hope for the best. I'm going to be moderate and cut my expenditures by 10%.

Posted in

|

2 Comments »

January 9th, 2007 at 07:41 pm

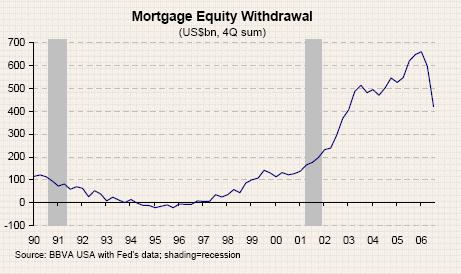

Source: Text is Sudden Debt and Link is http://suddendebt.blogspot.com/2007/01/some-rather-unpleasant-charts-chart.html Sudden Debt

The next chart shows how much money was taken out during the housing bubble in the form of equity withdrawal (the Fed estimates that 2/3 of this money was consumed - not saved). The amount is now going down fast and the impact is being felt in the retail sector.

I excised some text blaming the spending on plasma TVs.

Posted in

|

0 Comments »

January 9th, 2007 at 02:39 am

I checked Hugh Chou's Text is Retirement Savings Calculator. and Link is http://www.hughchou.org/calc/wealth2006.php Retirement Savings Calculator. For our age range, we're doing better than most retirement savers. We're not at the top end of the range (ages 35 - 44), so maybe we're doing better than 90% of the folks out there. 5% of the people in this group have $150,000 - $250,000 saved for retirement. And no, counting home equity for that is cheating.

We don't have mutual fund and stock brokerage account balances worth mentioning. Maybe I should start.

What's scary is looking at age groups beyond ours. Of all retired people, 20% have funds beyond $250,000. And we started to save only nine years ago. If we were smarter with our careers, and more driven and less poor, saving as soon as we got out of college and into those professional rather than support positions, we'd be surfin'! Our $$ includes the stock shock drops of 2000 and 2001.

Text is Hugh's got lots of calculators out there and Link is http://www.hughchou.org Hugh's got lots of calculators out there -- have fun.

Posted in

|

0 Comments »

|